Malaysian tax enforcement in 2020 - Updates

Following the recently concluded Special Voluntary Disclosure Program (SVDP) in September 2019, the IRB will increase its staff allocation for its enforcement activities from 60% to 80% in 2020. This is in line with its focus on tackling the issue of missing revenue from the shadow economy.

As reported by the IRB, collections from the SVDP amounted to RM 7 billion. This program was part of the Government’s tax reforms to encourage tax compliance. Meanwhile, the 2020 tax budget is set at RM 155 billion for taxes – a tall order for the IRB to achieve, considering the Coronavirus pandemic faced by our country and global community, with an imminent severe downturn in economic activity.

The IRB also recently issued the revised Tax Audit Framework 2019, Tax Audit Framework for Transfer Pricing 2019 and Tax Investigation Framework 2020. We understand that these updates are the IRB’s additional efforts to enhance higher tax compliance among taxpayers.

Tax audit framework, tax investigation framework and tax audit framework for transfer pricing

The revised frameworks are essentially similar to the earlier Frameworks, except for the incorporation of the following salient changes:

Audit procedures

|

|

Tax Audit Framework 2018 |

Tax Audit Framework 2019 |

|---|---|---|

|

Audit Procedures |

- IRB can make visits to the premises of a taxpayer or the taxpayer’s related business by giving notice in advance. - However, IRB may make visits to the premises of a taxpayer or the taxpayer’s related business without first informing the taxpayer. - Audit cases are to be completed in 90 days from the start of the date of audit visit. |

- The visits to the premises of a tax payer or the taxpayer’s related business without first informing the taxpayer has been removed. - In the absence of an audit visit, Determination of Commencement of Case Settlement Period Letter will be issued to the taxpayer to inform the commencement date for computation of the audit case settlement period. - Audit cases are to be completed in 90 days from the start of the date of audit visit or the date of Determination of Commencement of Case Settlement Period Letter is issued. |

Penalties

|

Penalty regime |

Audit Framework 2018 |

Audit Framework 2019 |

|---|---|---|

| Normal audit | ||

|

Offence under subsection 113(2) of the Income Tax Act, 1967 (ITA, 1967) |

100% of the tax undercharged. The Director General may use his power under subsection 124(3) of the ITA, 1967 to impose penalty of 45% on the tax undercharged. (Note1) |

100% of the tax undercharged. The Director General may use his power under subsection 124(3) of the ITA, 1967 to abate or remit the penalty imposed. (Note1) |

|

Repeated offence

|

100% of the tax undercharged for repeated offence in relation to a taxpayer which is under the Monitoring Deliberate Tax Defaulters Programme. (Note2)

|

55% of the tax undercharged. (Repeated offence in this case is in relation to a taxpayer who has been audited or investigated and the original, additional, or composite assessment with penalty under subsection 113(2) of the ITA, 1967 was raised. The first offence to be accounted for is from the date of the notice of assessment raised beginning 1 January 2020). |

|

|

Voluntary disclosure |

|

|

Offence under subsection 90(1) of the Income Tax Act, 1967 (ITA, 1967) |

Period from date of submission of returns ≤ 60 days = 10% > 60 days to 6 months = 15.5% |

N/A |

|

Offence under subsection 113(2) of the Income Tax Act, 1967 (ITA, 1967)

|

Period from date of submission of returns ≤ 60 days = 10% > 60 days to 6 months = 15.5% > 6 months = 35% |

Period from date of submission of returns ≤ 60 days = 10% > 60 days to 6 months = 15.5% > 6 months = 35% |

Note1: In practice, a penalty of 45% will be imposed for the first offence.

Note2: In practice, an additional 10% will be imposed for each repeated offence not exceeding 100%.

Investigation Procedures

|

|

Tax Investigation Framework 2018 |

Tax Investigation Framework 2020 |

|---|---|---|

|

Investigation Procedures |

- The IRB officers may visit the taxpayer’s business premises without first informing the taxpayer. |

- The IRB officers may request documents and information from the taxpayer, tax agent and third party. - The taxpayer may be required to provide information and oral explanations at the IRB’s offices. - The IRB officers may also visit the taxpayer’s business premises with written notification given prior to the visit. |

Tax Audit Framework for Transfer Pricing

|

|

Tax Audit Framework for Transfer Pricing 2013 |

Tax Audit Framework for Transfer Pricing 2019 |

|---|---|---|

|

Years of assessment covered |

5-year time bar |

7-year time bar |

|

Documents to be submitted prior to commencement of a field audit |

PowerPoint slides with details of the business during the audit opening meeting |

PowerPoint slides must now be provided to the MIRB at least 7 calendar days prior to the audit visit |

|

Timeline to furnish documents and information |

21 days |

14 days |

|

Deadline to respond to IRB’s proposed Transfer Pricing adjustments |

21 days |

18 days |

Penalties - Transfer Pricing

|

Penalty Regime |

Normal audit |

Voluntary disclosure |

|

|---|---|---|---|

|

Audit Frameworks 2013 |

Audit Frameworks 2019 |

||

|

No contemporaneous Transfer Pricing documentation (TPD) |

35% |

50% |

N/A (Note1) |

|

TPD not prepared in accordance to the requirements in the guidelines |

25% |

30% |

20% |

|

Failure to furnish TPD within 30 days upon request |

N/A |

30% |

20% |

|

TPD prepared in accordance to the requirements in the guidelines and furnished within 30 days upon request |

0% |

0% |

0% |

Note 1: Under TP audit framework 2013, the penalty rate for voluntary disclosure before the case is selected for audit is 15% (30% after the taxpayer has been informed but before commencement of audit).

Issues raised from tax authorities’ review

In conjunction with the IRB’s initiatives on its enforcement activities, the main issues raised by the Tax Authorities in relation to some of the recent tax audit and tax investigation cases are:

- High base assets (local and foreign): holding a lot of directorships and shareholdings, and having frequent local and overseas bank transactions are amongst the IRB’s targets.

- Evaluating the treatment on land transactions, i.e. Income Tax Act, 1967 versus Real Property Gains Tax, regardless of when the transaction occurs.

- Evaluating the nature of any payments made to non-resident and the date of crediting the payment.

- Evaluating the timing for income recognition, i.e. monies received in advance for future services and profit recognition by property developers or construction companies.

- Evaluating the basis of claims of any large tax deductions in relation to abnormal/extraordinary expenditure.

- Evaluating the cost components of management fees, i.e. mark-up percentage used in provision of management fee by service providers to the service recipients, and also on how these specific functions benefit the service recipients.

- Evaluating on the lower percentage of return on sales (i.e. cost plus mark-up percentage) in previous years of assessment as compared to the current year of assessment from the arm’s length perspective.

Customs audit – GST/SST

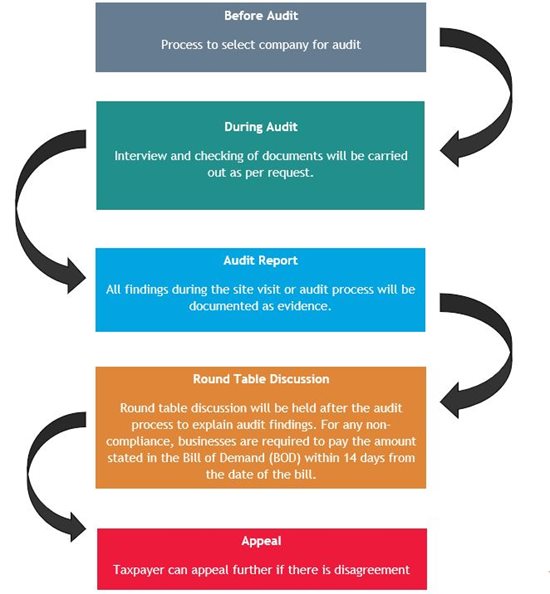

The Royal Malaysia Customs Department (RMCD) issued an Audit Compliance Framework on 30 April 2019 to ensure taxpayers comply with the relevant law and regulations.

Generally, RMCD’s audit procedures will be as follows:

Common issues during GST/ SST audit review

With Goods and Services Tax (GST) repealed on 1 September 2018, RMCD is actively conducting audit to expedite GST refunds to businesses. As of February 2020, RM 7.8 billion GST refunds are still owing to businesses. The Customs aims to complete all GST audits and refunds to businesses this year.

Some of the common issues we observed during GST audit are as follows:-

- Documentation not available;

- Reconciliation of forms submitted compared to Companies accounts; and

- Difference in interpretation of laws and regulations.

In addition, with the reintroduction of Sales Tax and Service Tax (SST 2.0) in September 2018, the Customs has started enforcement in conducting audit since early 2019 to ensure compliance of the businesses. Although the SST 2.0 is generally similar to the previous system (i.e. SST 1.0), there are still differences that businesses should note.

Some of the common issues we observed during SST audit are:

- Businesses are not aware that they are being auto-registered by Customs;

- Businesses used SST 1.0 model for SST 2.0 implementation;

- Businesses did not keep up to date with the latest changes; and

- Difference in interpretation of laws and regulations with Customs.

Summary

With the increase of IRB enforcement staff and issue of revised frameworks for tax audit and investigation, taxpayers who have not made voluntary disclosures face a higher possibility of being selected for audit or investigation at any time for prior years and the current year of assessment.

As such, taxpayers are encouraged to perform tax risk assessments to ascertain any potential Income Tax/GST/SST issues/areas (e.g. completeness of accounting records, related party transactions, individual net wealth analysis, GST/SST compliance, etc.).

It is important for taxpayers to prepare a checklist to cover the following in order to ensure that they are well prepared:

- Income, assets and liabilities listing for 7 years for the preparation of net wealth analysis and capital statements.

- Reconciliation of income and expenses (especially large amount) with supporting documents

- Cash sales reconciliation and controls.

- Documents to support land transactions as capital transactions, i.e. board resolutions, accounting records.

- Transfer pricing documentation to support related party transactions.

- GST details listing, sales and purchased invoices, GST return forms and reconciliations are in place to prepare for GST audit.

- Customs confirmation letter for certain transactions.

- SST system kept up-to-date with the changes of law.

Businesses are currently facing many challenges, so it would be advisable to be more vigilant and to keep abreast with the latest changes in law to ensure full compliance and avoid/mitigate penalties. In addition, all Malaysians and the Global community now face further uncertainties arising from the large-scale disruption to economic activity due to the COVID-19 pandemic.

Prevention is better than cure!

Christopher Low

chrislow@bdo.my