Repeal of tax-free importation of goods

Under current Norwegian law, importation of goods from abroad is, in general, free of duties and VAT, provided the value of the goods is less than NOK 350 including freight and insurance costs. This exemption, however, is not applicable for tobacco and alcohol.

As a result of the national budget for 2020, this tax exemption will be repealed in two steps: the first on 1 January 2020 and the second on 1 April 2020.

Changes from 1 January 2020

Beginning 1 January 2020, food, beverages, and other goods subject to Norwegian excise duties will be subject to excise duties and VAT no matter the value of the goods. As for tobacco and alcohol there will be no change, as these products are subject to excise duties today.

Changes from 1 April 2020

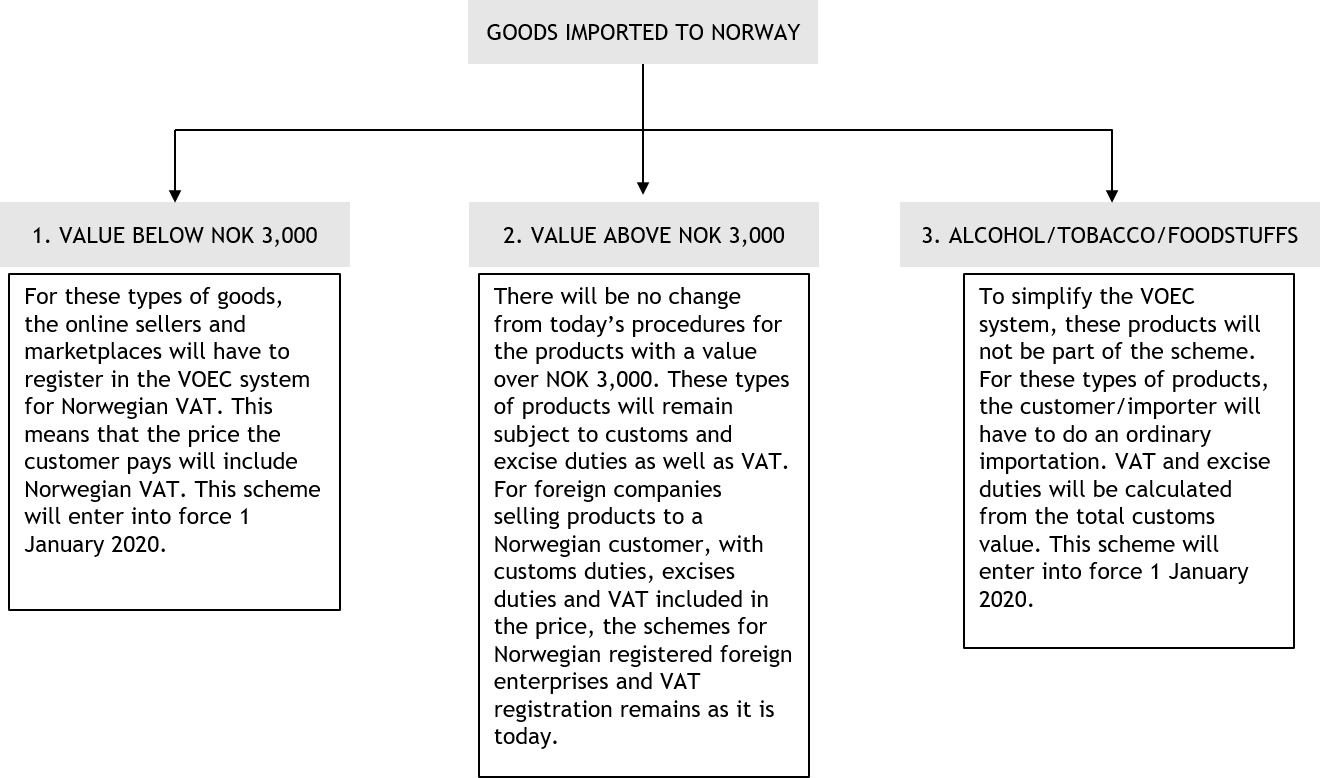

Beginning 1 April 2020, a simplified system will be introduced applicable to importation of goods other than those mentioned above whose value is below NOK 3,000[1] if those goods are sold via online sellers and marketplaces. Under this system, online sellers and marketplaces will have to register, declare, and pay output VAT on business-to-consumer (B2C) supplies of low-value goods (below NOK 3,000). The system will be implemented as an extension of the existing VAT on Electronic Services (VOES) system, that is, a simplified scheme for VAT on cross-border B2C sales of electronic services, which will be called the VAT on small consignments (VOSC). The collective name for the two systems will be VAT on E-Commerce (VOEC).

The VOEC is in accordance with principles set out in OECD guidelines. The proposal also has some similarities with the EU VAT e-commerce package that is to be effective 1 January 2021—in particular, the extension of the scope of the EU MOSS scheme to encompass distance sales of low-value goods imported from third countries and repeal of the current VAT exemption for imports of small consignments.

For foreign companies that align their marketing to target the Norwegian market, the registration requirements according to the Norwegian VAT law is still applicable. When these companies reach a turnover of NOK 50,000 they will have to register for VAT and invoice Norwegian customers with VAT.

Different scenarios

Conclusion

Given these changes, we recommend foreign companies supplying goods to the Norwegian market assess how their activities should be structured as of 2020.

Knut Andreassen

knut.andreassen@bdo.no

Helene Hval

helene.hval@bdo.no

[1] Approximately EUR 300