Our 6 August 2020 Insight depicted a future of increased tax authority investigations as a side effect of the need for governments to raise tax revenues. Greater corporate taxes may help reduce fiscal deficits as the world emerges from the COVID-19 pandemic-induced economic crisis. Yet tax authorities can only enforce legislation as it exists today in the short-term, so many governments have been advocating for fundamental reform of tax regimes to yield more tax from business.

The OECD and its Inclusive Framework of 137 countries are rapidly developing two new models for how international businesses pay corporate tax. The first model – Pillar 1 - affects highly digital and consumer-facing businesses. Rights to tax profits would shift in part from countries of production (or development) to countries of consumption, based on yet-to-be-agreed formulae. The second model – Pillar 2 – affects all sectors through reformed tax laws that would require income to be taxed at a minimum effective rate. In simplest form, Pillars 1 and 2 allow one country to tax business profits earned in another country. When it comes to their detail, the two Pillars have little in common.

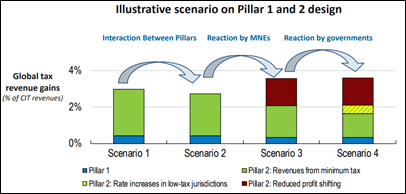

Since the OECD kicked off this project in early 2019, Pillar 1 has so far received greater attention than Pillar 2. Then, analysis published by the OECD in 2020 showed that Pillar 1 will largely be a redistribution of tax revenue and that the global tax revenue gains from Pillar 2 far outweighed those from Pillar 1 (see following diagram). And, while the OECD and participating governments intend to progress both Pillars in tandem, agree all key criteria and develop their legislative blueprints, multi-lateral consensus will be fundamental to worldwide adoption of Pillar 1, while tax legislation to implement Pillar 2 can be enacted quickly by individual governments without international consensus. We therefore advise tax leaders begin to pay closer attention to Pillar 2 and derivative tax law changes in key jurisdictions.

Diagram 1

Source: OECD Update on Economic Analysis and Impact Assessment (February 2020)

What is Pillar 2?

Pillar 2 - referred to as Global Anti-Base Erosion or “GloBE” – is an international tax framework where countries can tax income earned in other countries if that income is taxed below a minimum effective rate. At present, GloBE should affect international businesses with consolidated revenues above €750 million or equivalent, as the OECD intends to mirror the revenue threshold set for country by country reporting (CBCR) obligations.

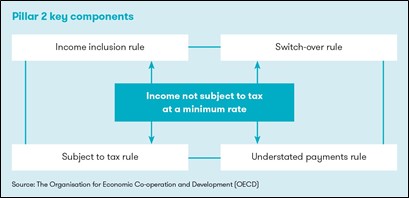

GloBE comprises two core rules over the right to tax income in a different country.

- Income inclusion - the parent entity pays a “top-up” tax in relation to insufficiently-taxed income earned by its foreign subsidiaries and branches,

- Base-eroding payments - the entity making a payment is either denied a tax deduction or liable for a withholding tax when the foreign recipient is insufficiently taxed.

These core rules of GloBE break down to four inter-related rules shown in the following diagram. Conceptually, GloBE adopts existing international tax regimes. The income inclusion rule in GloBE mirrors Controlled Foreign Company (or Corporation) (CFC) tax rules, and CFC regimes have been in effect for decades. Withholding taxes and denied deductions for base-eroding payments have been universally adopted and coincide with the second GloBE rule. In effect, GloBE takes existing tax laws that curb aggressive tax planning and augments them to penalise low-tax outcome by any means. In all, GloBE intends to limit the effectiveness of low corporate tax rates as well as many tax incentives.

Diagram 2

What might concern business?

Business leaders should care about two likely outcomes from GloBE: (1) De-legitimised sound tax incentives, and (2) Double tax. GloBE is about ensuring all businesses pay a minimum effective rate of tax on all income earned. GloBE’s current form will minimise the attraction for purposeful and non-harmful tax incentives. Many of these encourage business investment in research, innovation and environmentally-conscious projects. If GloBE de-legitimises those incentives, businesses may decide to invest less in these strategic areas.

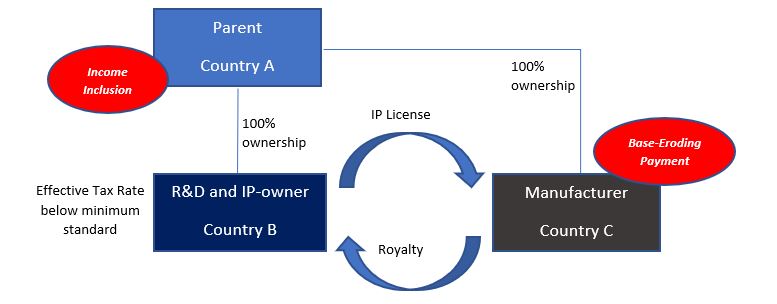

For double tax not to occur, the GloBE framework must enforce a strict hierarchy of taxing rights. Consider an example where tax is paid by an R&D and IP-owning subsidiary at below the minimum effective rate in Country B. GloBE will permit Countries A and C to claim taxing rights to the same income in Country B under their domestic legislation, through the income inclusion rule for Country A and through the base-eroding payments rule for Country C. Unfortunately, current tax treaty frameworks do not reflect the interaction between Countries A and C because there is no direct transaction between the entities in Country A and Country C. If governments introduce local instances of the GloBE tax rules quickly to raise revenues without mechanisms to prevent double tax, such as updated tax treaties, businesses could suffer multiple layers of tax on the same income.

Diagram 3

What should businesses do?

Changes to structures or transactions are not recommended until the OECD or individual countries set out clear and definitive rules. That said, GloBE’s core objective lends itself to a simple risk-assessment for business. The GloBE framework targets under-taxation in any jurisdiction. Ultimately, the group in the above illustration will pay more tax under GloBE, whether it is paid to Country A or C. It may be important today for a global business to estimate the incremental tax cost from GloBE if at least a minimum rate of effective tax were paid in each jurisdiction in which the group operates. The minimum rate itself remains an undecided point within the OECD and its Inclusive Framework. For now, businesses may want to estimate its GloBE tax bill by modelling minimum tax rates from 10% to 15% (OECD economic impact depicted in Diagram 1 was computed by assuming a 12.5% minimum tax rate).

Some international businesses will maintain robust financial and tax data to model changes to effective tax rates by entity or country. Alternatively, those businesses covered by Pillar 2 should have prepared and filed CBCRs. These reports disclose pre-tax income as well as corporate income tax accrued and paid by tax jurisdiction. While CBCR data will not yield the precise effective tax rate in-line with Pillar 2 rules, it can generate a best estimate for a risk-assessment.

What is next?

While most international businesses remain focused on the commercial impact of COVID-19, tax leaders must acknowledge the appetite for countries to introduce GloBE-inspired tax legislation as early as 2021.

The OECD has developed draft blueprints for both Pillar 1 and 2 in advance of the October G20 Finance Ministers and Inclusive Framework meetings. Significant progress will need to be demonstrated at the meetings in order to achieve consensus for all material design and implementation aspects. In spite of progress the OECD may demonstrate, and certainly if progress and consensus are not demonstrated, the economic impact of COVID-19 may press some countries to accelerate tax-raising measures. Certainly, if the OECD cannot evidence satisfactory progress in 2020, business should anticipate even more unilateral tax measures to be rolled out during 2021.

Subscribe to receive the latest BDO News and Insights

KEY CONTACT

Head of Transfer Pricing, Ireland

Please fill out the following form to access the download.