New technology developments stimulate e-commerce investment and growth

New technology developments stimulate e-commerce investment and growth

Technology is driving funding and deal activity in the e-commerce space. As commerce continues to move online, new solutions and M&A strategies are coming to the fore. Headless e-commerce and marketplace aggregation are two of the prime examples.

Technology is driving funding and deal activity in the e-commerce space. As commerce continues to move online, new solutions and M&A strategies are coming to the fore. Headless e-commerce and marketplace aggregation are two of the prime examples.

In the early parts of 2020, many of us started seeing a lot more to e-commerce delivery drivers. As the COVID-19 pandemic swept across continents, online shopping saw an unprecedented burst of growth. For example, in America, where US Census Bureau data show e-commerce, as a percentage of all retail sales, rose from 11.8% in the first quarter of 2020 to 16.1% in the second quarter. Similar developments were seen across the world.

BDO’s 2021 Retail Forecast Report summarises the developments thusly:

“Physical stores and discretionary sectors that were significantly impacted by the direct and indirect effect of the (COVID-related) restrictions, such as clothing, beauty, and big-ticket home items, saw much bigger declines (in sales)[…].In contrast, online retailers and retailers of food and several other niche categories, were faced with unprecedented opportunities.”

Data: eMarketer, Graph: BDO Global.

Analysis from eMarketer shows that the worldwide average YoY growth in e-commerce retail sales for 2020 was 27.6%.

Across industries, companies are proactively adapting to the new reality. In the 2021 Retail CFO Outlook Survey, 71% of CFOs say that they will increase IT investments during 2021. 64% say that they plan to increase investments in e-commerce over the coming six months.

The lesson is that online sales channels are no longer an option but a necessity. Customer behaviours and preferences are changing, and keeping up requires flexible online solutions. For the e-commerce sub-industry, and related spaces like retail technology, the changes have increased the momentum of and investment in new technological approaches, such as headless e-commerce, and new acquisition strategies, like marketplace aggregation.

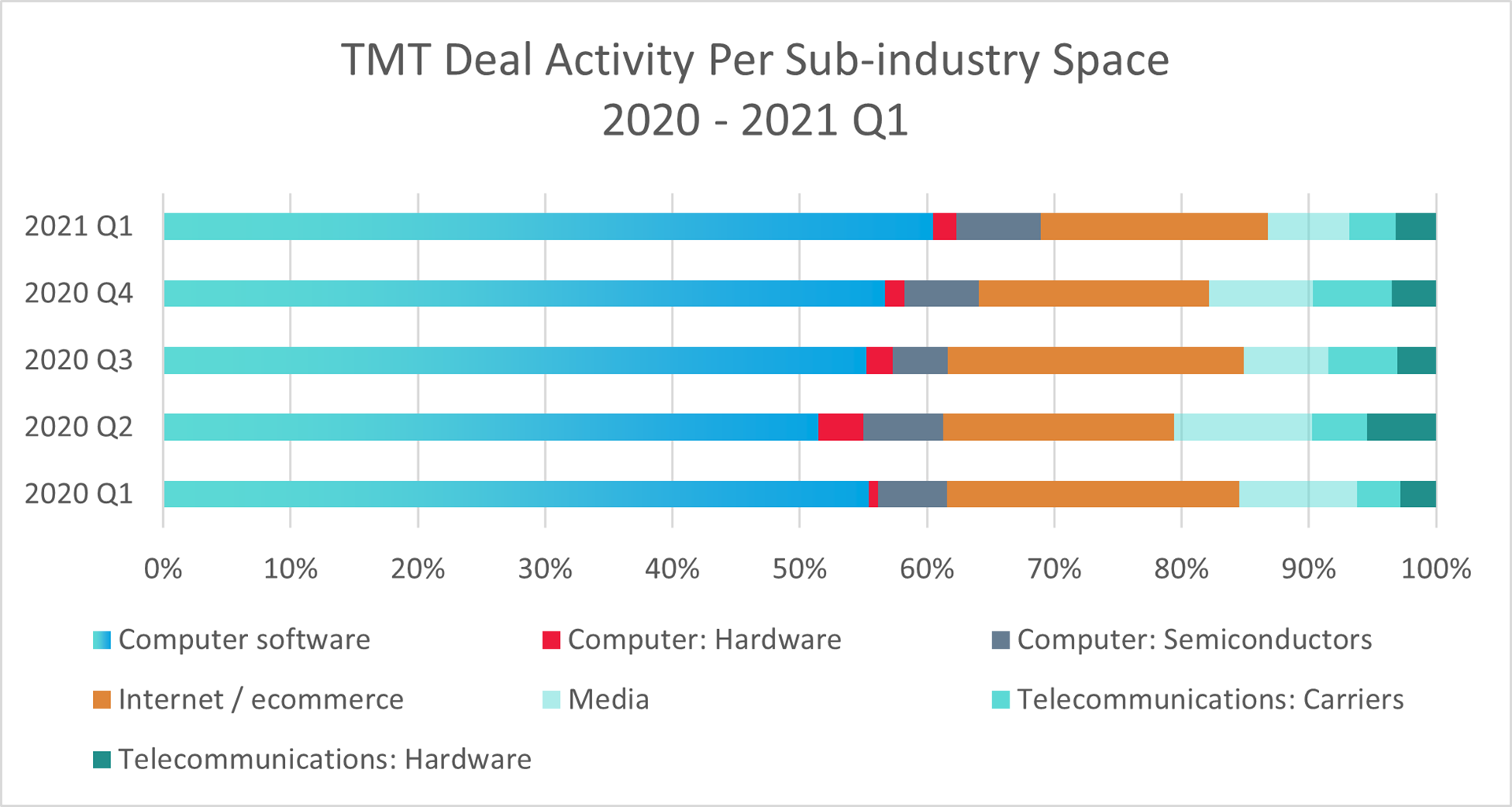

TMT Remains in the M&A Driver’s Seat

BDO M&A analysis shows that e-commerce was one of the drivers behind a robust 2020 and start to 2021 for mid-market technology, media, and telecoms (TMT) M&A.

A busy Q4 2020 saw a flurry of 515 completed mid-market TMT deals. 2021 continued the trend with 438 mid-market Q1 deals (one of the strongest first-quarter performances in recent times). While slightly down from Q4 2020, the backdrop of a more marked M&A slow-down for other industries underscores TMT’s resiliency, strong market prospects, and continued investor interest. If deal activity continues, 2021’s TMT deal total will eclipse 2020.

.png.aspx?lang=en-GB)

Data, graph: BDO Global

Private Equity’s (PE) TMT appetite remained strong. There were 154 PE buyouts in the first quarter (equalling 35.2% of deal volume and 46.6% of deal value).

Total deal value across all TMT mid-market deals topped US$51 billion, just beating 2020 Q4 and solidly outperforming previous quarters.

Data, graph: BDO Global

Within TMT, software (265 deals) dominated activity followed by Internet / e-commerce (78 deals).

Shopping Moving Online

Analysis predicts that e-commerce will account for between 18% and 19% of total retail sales in 2021, reaching 22% by as early as 2023. While other analysts set the growth slightly lower, developments in the world’s biggest e-commerce markets show a uniting trend of solid spending growth throughout 2019 and 2020, predicted to continue through 2021.

Data from BDO’s global retail teams indicate that the increase in online retail is here to stay.

Analysis performed with BDO USA's proprietary Forecast Engine on over 20,000 estimates for 419 public companies spread across 24 industries shows online retail to be least impacted and showing best performance in EBIT Changes vs TEV Performance. Online retail also topped performance for long-term EBIT forecasts with a 26% growth in forecasts between February 2020 and January 2021.

.png.aspx?lang=en-GB)

Perhaps the changes were best coined in the latest edition of BDO UK’s High Street Sales Tracker, which includes April when UK stores fully reopened:

“According to BDO’s High Street Sales Tracker (HSST), non-store like for like sales grew by +28.2% in April from a base of +109.6% last year, a remarkable result given last year’s record increase in online spending during the first nationwide lockdown. With online sales continuing to hold up even after shops have reopened, the result suggests both a rebound in consumer confidence and discretionary spending but also that shifts in consumer behaviour towards greater online shopping are ‘sticking’. “

Globally, e-commerce revenue is led by China, which supposedly now sees more spending online than in-store – a trend that could soon extend to other large economies. Despite the US remaining just ahead of China in overall retail sales (US$5.506 trillion vs US$5.13 trillion in 2020), Chinese online e-commerce outpaced the US by nearly US$2 trillion. The growth is expected to continue, with combined global e-commerce spending set to reach US$6.54 trillion by 2022.

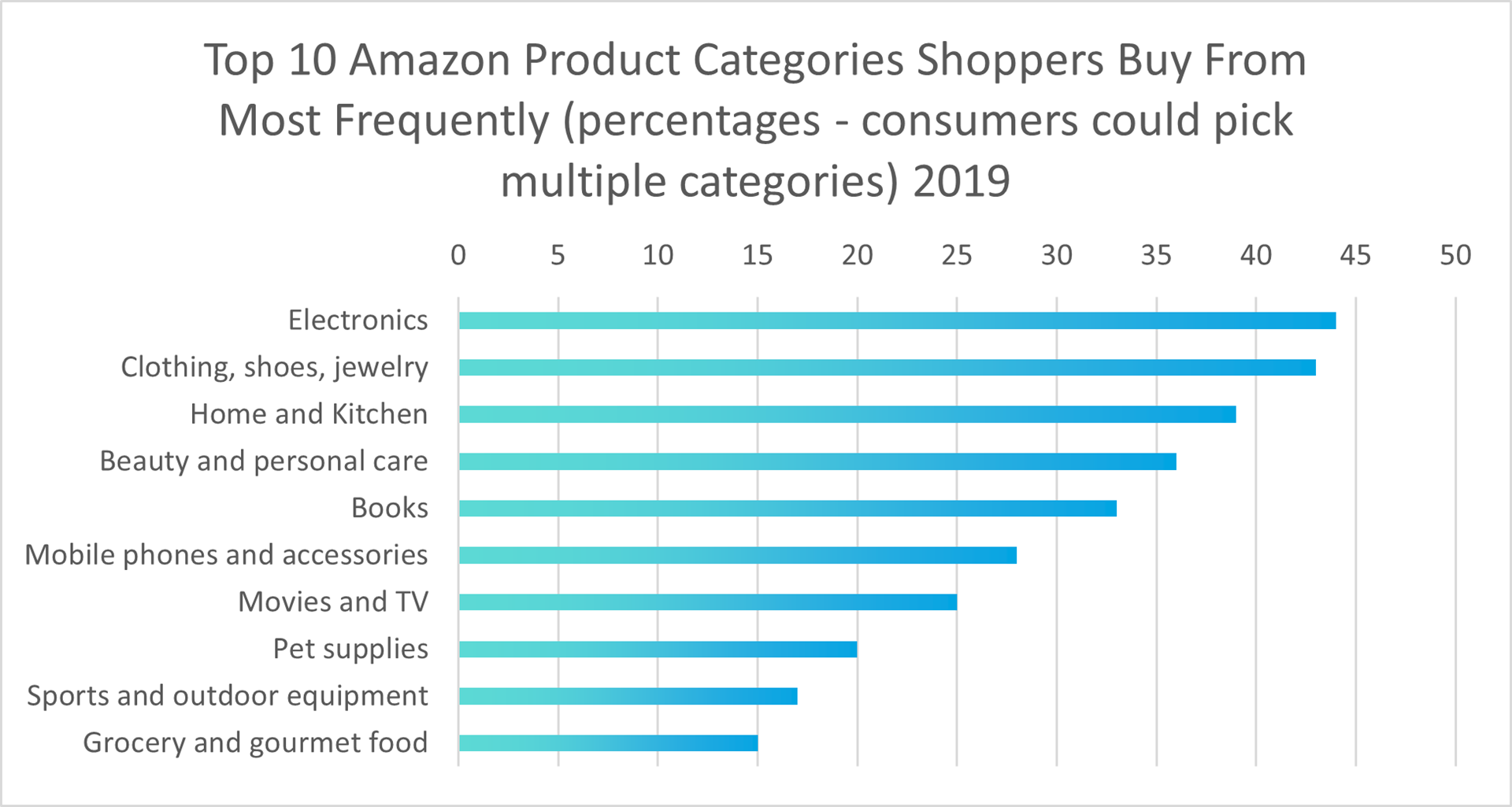

Data: Feedvisor, Graph: BDO Global

E-commerce extends to all types of retail sales, and a Feedvisor study of the most popular product categories (B2C sales) on Amazon shows how broad our tastes for online shopping have become.

Online shopping is more popular than ever across all customer segments, but doubly so with younger generations. One study found that millennials do more than 60% of their shopping online.

Technology’s Role in Growth

Many stores and enterprises probably view Amazon as retail’s answer to Pacman - an entity that gobbles up all customers and sales. However, that is far from the case. Otto Group, Zalando, eBay, Tesco, Veepee, Bol, Walmart, Flipkart, Alibaba, Shopee, JD, Etsy, and Rakuten are just a few other major online shopping entities. Furthermore, more than 50% of global e-commerce happens through other channels than online marketplaces.

In other words, stores and companies across sizes and industries have many different ways of using technology and new solutions to interact with its customers and stay relevant to customers’ evolving preferences and needs.

Data: CB Insights, Graph: BDO Global

Across retail, examples abound of companies proactively acquiring and leveraging new e-commerce and retail technology in different ways, including:

- Condé Nast’s in-video feature that allows viewers to purchase apparel worn on screen – for example, in Vogue’s “7 Days, 7 Looks” series.

- L’Oréal leveraging its acquisition of AR company Modiface to launch features that enable users to try its products virtually from home through an app.

- Asos partnering with the Israeli technology company Zeekit in a trial of technology that lets users try on clothes online.

- Zara using advanced AI and big data analytics to predict clothing trends and minimise waste.

As Uniqlo CEO Tadashi Yanai often says: “Uniqlo is not a fashion company, it's a technology company.” When looking at technology solution investments across retail, that mindset is clearly shared by many other companies.

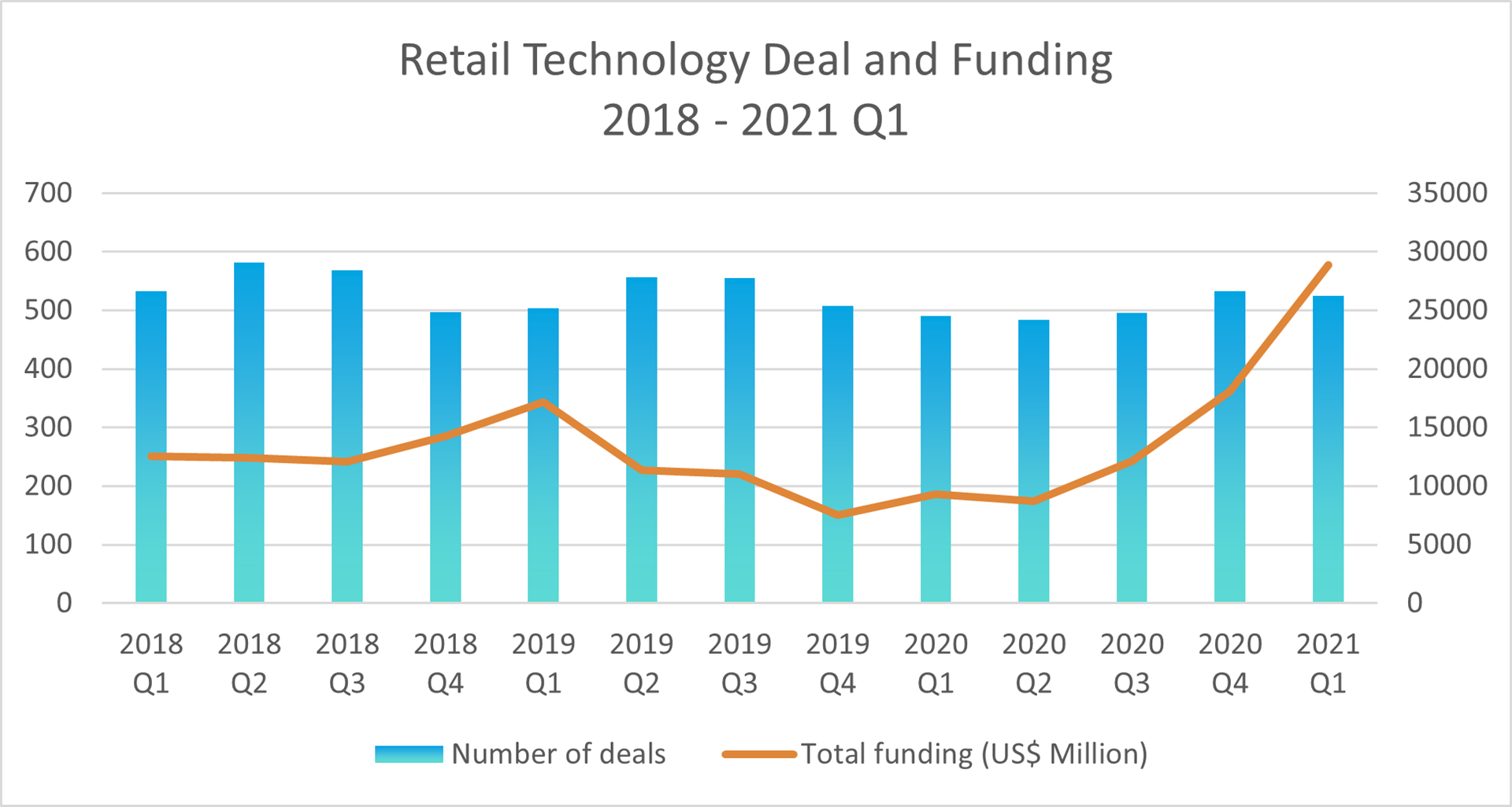

E-commerce M&A and Funding on the Rise

Evolving consumer and seller needs, along with technological development, have also driven e-commerce M&A and funding activity. Across all market segments and company sizes (from start-up to multinationals), there was a record 794 mergers and acquisitions involving the likes of e-commerce software, platforms, and marketplaces in the first half of 2020.

Data: Crunchbase, Graph: BDO Global

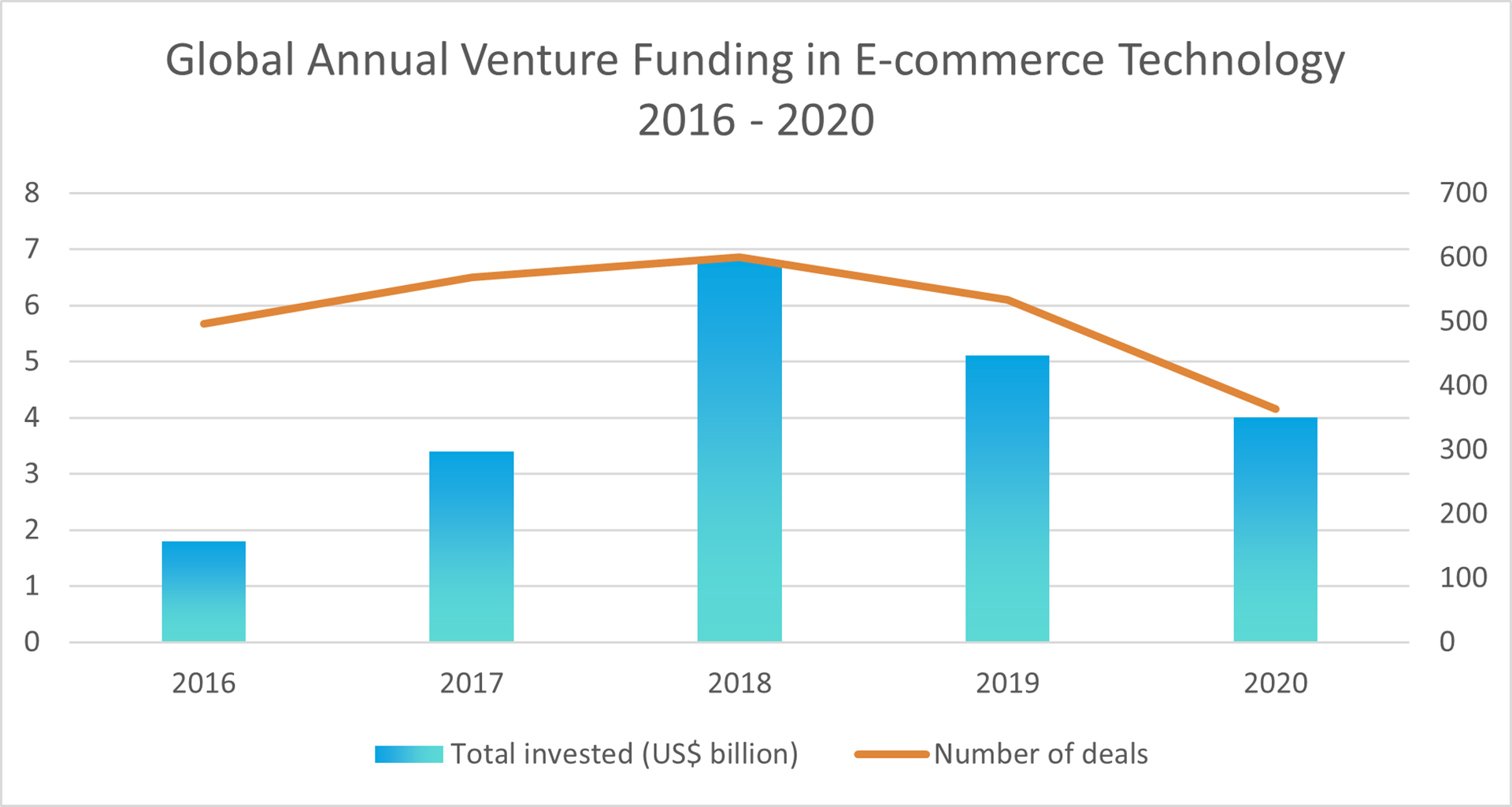

VC activity in the space has seen a fall in recent years. However, while 2020’s total VC deals and combined deal value were somewhat down, the average deal size rose to US$11 million, compared to US$9.5 million the previous year.

It should also be noted that, as detailed earlier, total deal value and deal numbers across the space rose in 2020 and into 2021. The developments could potentially be an indication of PE and retail companies themselves increasing deal and funding activity. The latter corresponds with the findings of BDO’s Retail CFO Outlook Survey.

M&A and funding drivers include industry consolidation, the emergence of new sub-industries, new technology, and increased competition over the growing market for e-commerce solutions and related infrastructure. As a result, e-commerce providers are looking to match competitor offerings and differentiate themselves – in part through acquisitions.

The latter is also a trend in related spaces, such as delivery and last-mile technology, which saw scale-ups looking to build out their positions by raising growth capital throughout 2020. Examples include Turkish start-up Getir raising US$300 million, German start-up Gorillas raising US$290 million and Finland’s Wolt raising US$530 million.

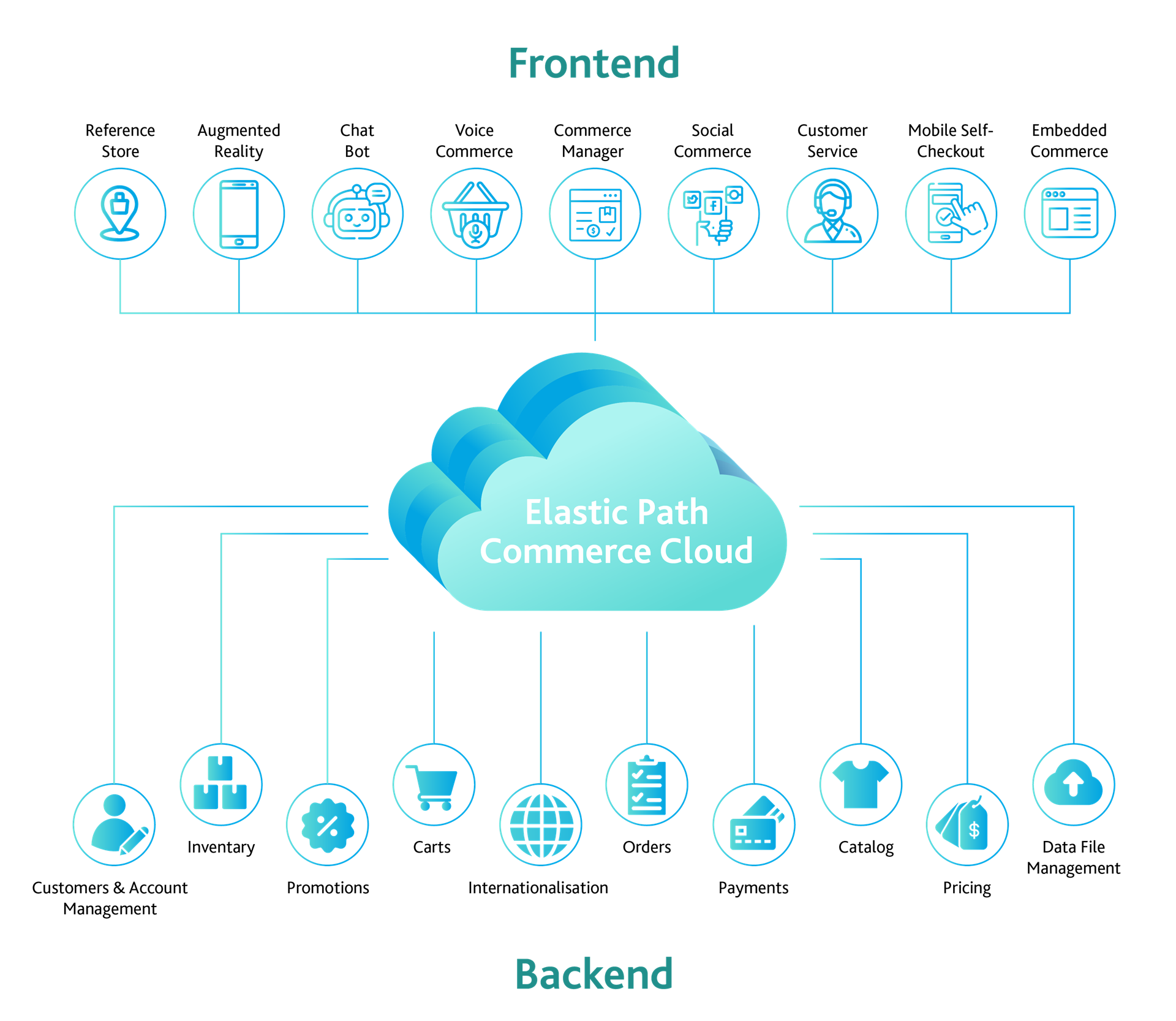

E-commerce Going Headless

While Amazon still dominates, e-commerce is changing rapidly. In 2020, Amazon captured 31.4% of all US e-commerce retail sales, down from 43.8% in 2019, according to Digital Commerce 360.

One reason is that more companies are investing in unique, stand-alone online sales platforms. Some choose to invest in end-to-end platforms or in-house development. However, downsides of these approaches can include slow go-to-market timelines, low sales channel flexibility, and high development costs.

Another approach is headless e-commerce architecture, which has seen increased media and market interest.

In headless e-commerce, customer interfaces (frontend or presentation layers) like storefronts and device type-specific design are separated from core commerce functions (backend or application layers) like payment processing and inventory tracking. The two are connected through APIs.

The approach can offer brands and retailers easier, more flexible sales channel roll-out and optimisation of tailored shopping experiences through a multitude of mediums, including voice, text, social media, web, and mobile. Achieving these qualities can be complex – especially for small to mid-sized enterprises – through in-house development or end-to-end solutions.

Headless Funding and M&A Picks Up Pace

2020 and 2021 have seen headless e-commerce funding and M&A on the rise. Funding examples include Fabric landing a US$43 million Series A and Webscale closing US$26 million in growth capital. In total, headless e-commerce companies have raised US$1.2 billion in funding over the last two years.

The space is also seeing bolt-on acquisitions and moves aimed at merging headless with existing offerings. Headless e-commerce vendor Chord acquiring Denver-based e-commerce data start-up Yaguar and cloud company Sitecore acquiring headless e-commerce company Four51 are two examples. Big tech companies are also making headless M&A plays, such as CRM giant Salesforce’s purchase of Mobify for US$60 million.

Many are trying to emulate one of the most successful established online storefront vendors offering headless e-commerce solutions, Shopify. The company saw 38% YoY growth in consumers buying from companies using its solutions.

Perhaps the potential of headless e-commerce is best exemplified by Amazon investing in going headless, in part by acquiring Selz. The Australian headless e-commerce platform helps small businesses create sales channels similarly to how Shopify works.

Amazon Marketplace Roll-ups

Another driving M&A trend in e-commerce is acquisition companies focusing on roll-ups of Amazon sellers. The business model involves buy-outs and scaling sellers that are already successful on Amazon. This is partly achieved through cost-saving synergies, leveraging data analytic abilities, and integrating lessons learned throughout the ecosystem of acquired Amazon sellers to increase sales and profitability.

Since 2017, third-party sellers have represented more than half of Amazon gross merchandise sales, with the platform’s third-party marketplace ecosystem generating between US$25 billion and US$39 billion in profits in 2020, making them prime targets for companies able to scale their operations. Oftentimes, the buyer can lower the product price due to its ability to buy stock in bulk.

Data, graph: BDO Global

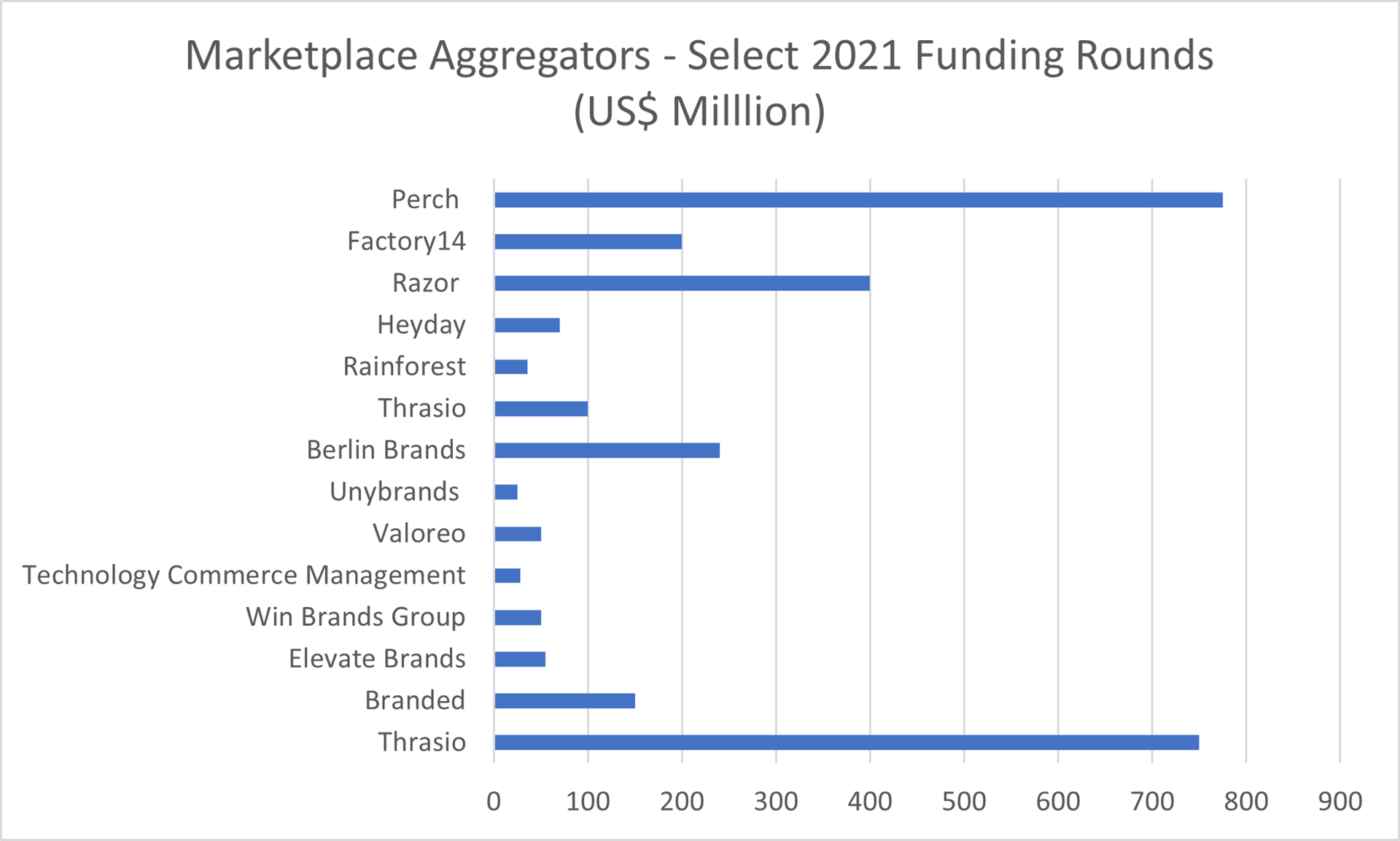

E-commerce aggregators, as the acquiring companies are often referred to, are seeing interest from investment banks, venture firms and private equity shops. Thrasio, one of the biggest companies in the space, recently announced that it had raised another US$750 million. It has to date acquired nearly 100 Amazon sellers.

The competition in Amazon marketplace roll-ups is heating up and seeing new entrants on an almost monthly basis. Other raises include SellerX’s US$118 million seed round. The raised capital will be deployed to buy up and grow Amazon marketplace businesses. By end of February 2021, e-commerce aggregators had raised a total of US$2.3 billion. Since then, activity has continued at ever-increasing speed. Thrasio has raised a further US$100 million, Razor US$400 million, Heyday US$70 million, Berlin Brands US$240 million, and Perch US$775 million. Combined, marketplace aggregators have raised around US$2.4 billion in March through May of this year alone.

With the speed of funding and market growth across retail tech and ecommerce tech in mind, we expect to continue to see increased M&A activity. Simultaneously, increased competition will be a factor in raising the importance of timely, detailed, and efficient deal negotiations, including areas such as due diligence and deal and tax structuring. These areas should be top-of-mind for both sellers and buyers to ensure optimal M&A outcomes.