Will cloud-native finish what Skype and WhatsApp started?

Will cloud-native finish what Skype and WhatsApp started?

New technology may outdate massive 5G investments before the next-generation networks are even completed. Along the way, technology and cloud companies could emerge as direct competitors to telecoms.

New technology may outdate massive 5G investments before the next-generation networks are even completed. Along the way, technology and cloud companies could emerge as direct competitors to telecoms.

Earlier this summer, Dish found itself in a race against time. In May, its cloud-native “Smart 5G™ network” officially launched in Las Vegas. To meet government requirements as the fourth US service provider of 5G, it had to expand services to cover 20% of the country’s population by mid-June.

In fact, Dish’s new network is a shining example of the risks identified in BDO’s 2022 Telecommunications Risk Factor Survey. The top five industry-specific risks identified include intense and increasing competition and rapid technology substitution.

In short, Dish’s network illustrates how cloud companies are an incipient threat to the telecommunications industry.

Outside antennas and cables, Dish’s network will almost exclusively live in Amazon Web Service’s (AWS) cloud systems. The network promises to be cheaper to set up and run and enables broad automation.

.png.aspx?lang=en-GB)

If Dish’s new network proves a success, it heralds a fundamental change to the global telecoms market.

Simultaneously, it will bring telecoms and cloud operators closer together. In the process, it may leave telecoms open to technology companies “eating” large chunks of the industry, similarly to how they have chewed their way through taxis and the film industry – not to mention the revenues telecoms used to generate from text messaging and international calls.

5G goes fully cloud

Cloud-native means a clean break with previous network generations. It enables deployment of 5G without relying on pre-existing 4G LTE RAN and core network infrastructure, which can limit network flexibility and incremental 5G functionality.

For telecoms, deploying 5G in a standalone format opens a range of advantages:

- Enhanced functionality: reduced downtime and streamlined deployments.

- Better scalability and flexibility: IP networks with capabilities surpassing traditional chassis-based routers and the flexibility to run cross-vendor software.

- Instant updates: software-centric containers and microservices mean that new functions or updates can be supplied by the software developer and added within milliseconds without interrupting service.

- Lower deployment costs: expensive infrastructure can be replaced with simpler hardware that links directly to cloud services.

Relying on existing infrastructure means that updates and scaling network capacity can take weeks or months and comes with a heavy price tag and downtime.

Cloud-native 5G enables integrating and deploying services similarly to how Uber, Netflix, and Facebook leverage cloud services, continuous deployment, elastic scaling, and automation in their business models.

Previously, deploying ‘pure’ 5G networks has been associated with heady installation costs. However, cloud-native changes that.

Dish’s solution provides a perfect example: its 5G network consists of sleek antennas and small base stations. Data picked up by the antennas is immediately linked to Amazon’s cloud services, effectively outsourcing data operations in much the same way many businesses use IT, software-as-a-Service and cloud-services providers. The combination makes the network cheaper to set up and manage. It will also be fully automated, right down to the virtual “labs” where new services are tested.

Is pure 5G the future?

With literally minutes to go, Dish squeezed past the wire and pronounced it had succeeded in reaching a fifth of the US population.

In the process, Dish, best known as a satellite pay-tv provider with 11.3 million subscribers, became a direct competitor for the revenues that AT&T, Verizon, and T-Mobile have been banking on to fund the $100 billion they have already spent on deploying 5G technology.

So far, Dish has spent around $2 billion to cover 20% of the population. It is expected to spend a total of $10 billion and leverage collaboration agreements to extend its coverage.

Its initial network is available on a limited number of devices that will be extended over time. However, it already leverages innovative technologies such as eSIM and multi-SIM, voice over new radio (VoNR) and 5G broadband 3GPP Release 15 enhanced mobile broadband (eMBB).

The company’s business strategy revolves around the potential that 5G holds as the foundation of the future of communications.

Driverless cars, smart city infrastructure, the Internet of Things, digital twin production lines and a whole host of other technologies will rely on rapid, low-latency data exchange and fluid scalability. These happen to be among cloud-native 5G’s core qualities.

In addition, companies and organisations are looking to invest in private, secure networks that can meet strict data protection requirements with predictable, stable performance.

According to ABI Research, nearly 90% of global enterprises will have migrated at least a quarter of their network infrastructure to a Network-as-a-Service model (NaaS) by 2030. By then, the NaaS market could be worth as much as $150 billion with telcos, provided they have the ability to capitalise, able to snag up to $75 billion of that sum.

Collaborations and M&A drive 5G developments

While Dish seems to have stolen a march on its competitors and their existing 5G investments, it is not alone in working on making cloud-native the foundation for the future of networks.

AT&T is among the companies pursuing similar solutions. The telecom giant made a splash by selling its cloud software stack and IP to Microsoft and using the company’s Azure for Operators hybrid cloud. AT&T also has an agreement with Google on developing 5G edge computing solutions.

Verizon has struck similar agreements with Ericsson and IBM’s Red Hat, while T-Mobile is partnering with Cisco and Ericsson on its cloud-native initiatives.

Google, Amazon, and IBM are all using their positions in the public cloud as a springboard to capitalise on the demand from business customers for 5G services.

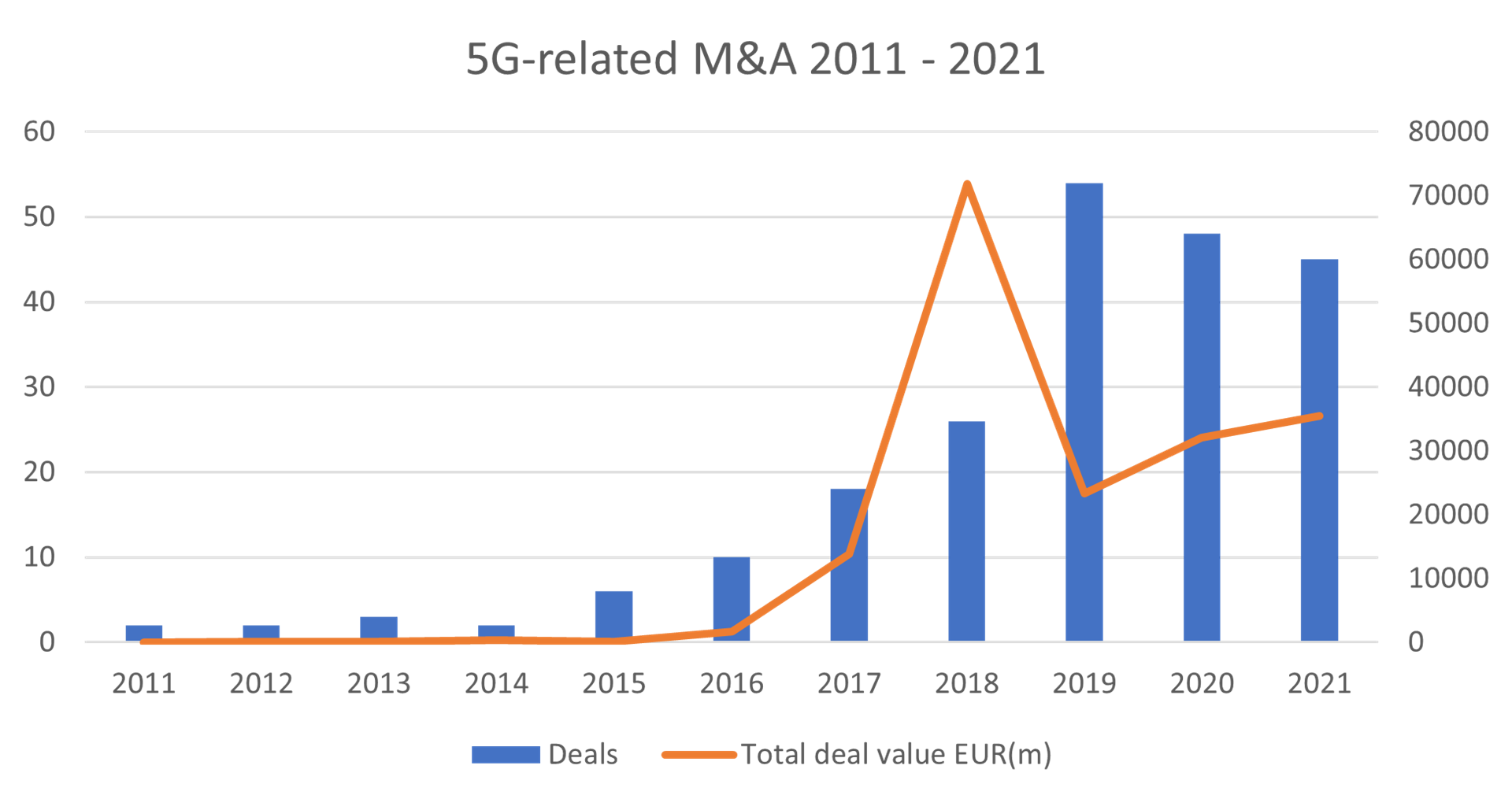

The developments indicate how major cloud providers are moving further into the telecom realm. The moves include M&A, such as Microsoft’s acquisition of Affirmed Networks and Metaswitch and Google’s acquisition of MobiledgeX.

Data: Mergermarket. Analysis and graph: BDO Global.

Mergermarket M&A data shows that Microsoft and Google are far from alone in making 5G-related acquisitions. Both deal totals and cumulative value have been rising in recent years (2018’s total deal value includes T-Mobile’s $26 billion acquisition of Sprint).

Tech companies readying to become telecoms?

The plethora of collaboration agreements and M&A activity indicate several things about telecoms and 5G:

- Telecom cloud, especially its “edge” (base station-level operations), is an area where telecoms have struggled to match technology companies in terms of technical developments, expertise, and scaling capabilities.

- Telecoms are partnering with technology and cloud companies to speed up the deployment of 5G, especially cloud-native 5G. Partnering with several technology providers is a preferred strategy.

- Increased 5G-related M&A activity seems to include acqui-hires, indicating a dearth of available talent and increased competition for 5G-related services, service providers and developers.

The alliance between telecoms and tech is an uneasy one: cloud companies have the technological edge. Telecoms, on the other hand, have customer relationships and own the radio spectrum.

However, technology companies are in a strong position to expand to cover (or eat) many more wireless networks.

At its core, cloud-native 5G is a software-based telecoms network separated from the hardware elements through virtualisation. This type of separation and software-based functionality may sound familiar to telecoms executives who remember what WhatsApp and Skype did to revenues from text messaging and international calls.

In other words, technology already ate telecoms’ lunch a decade ago – now they could be coming back for their dinner too.

Microsoft – incidentally, the owner of Skype – provides a good example of how the changing market dynamics and emerging technology may lead to further changes. Last year, it announced a private wireless network initiative with Nokia, which seems to take direct aim at the $75 billion NaaS market that telecoms have been eyeing with keen interest.